Archive for the ‘Chris’ Blog’ Category

Posted on: August 8th, 2017 by Chris Scott

I hope everyone is having a great summer so far. Our local housing market continues to impress. In July the market was once again well ahead of where we were this time last year. Let’s look at the numbers.

These are the average numbers. There are some areas that are experiencing double digit increases over the same period last year. Anything West of downtown to Carlingwood would be in this category. Buyers want to be central and are willing to pay a hefty price to get there. Take Westboro/Carlingwood areas as an example. The average price here for a single is $758,000 that is up 11.5% from a year earlier.

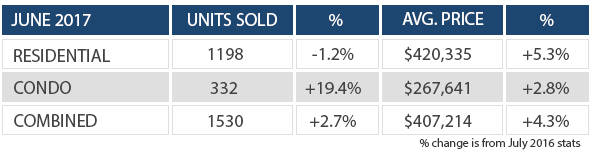

Another reason for the strength in our market is that condo market is making a comeback. Much of the inventory that has been stale the last few years is being sold off. This has really helped to strengthen the market as a whole. Many condo owners (myself included) have rented their condos in the past few years waiting for better selling conditions. The time might be right to list for those condo investors. The condo market sold 332 units in July 2017 which is an increase or 19.4% compared to last years July.

Inventory continues to be an issue in some locations-especially in the central areas. The amount of new listings coming to market is lower than the 5-year average. Buyers are still patiently waiting for properties to come available. We are seeing a more active summer because many buyers were unable to secure their home in the Spring.

Interest Rates could be a factor moving forward. As our economy strengthens it is natural that our key interest rate will rise. After many years of steady rates, we have finally seen a rise in the Bank of Canada rate. It recently increased by a 1/4 of a percent. Lenders have since followed suit. This will add about $12 more per month on average for every 100k of a mortgage. It will affect affordability but not enough to cool the Ottawa housing market. Something to keep our eye on. Ottawa is such a spread out city. There are different market trends happening in each micro market of the city. If you are curious to whats happening your neighbourhood let me know. I would be happy to provide you with a list of Ottawa homes that have recently sold around you.

Posted on: July 31st, 2017 by Chris Scott

The real estate market in Ottawa is often a very competitive place to purchase real estate. When a house is listed that shows well and is priced aggressively it will often attract more than one buyer. This creates a multiple bid situation. I have been in this situation too many times to count. Twice in the last week! In many of the cases, my clients are the ones who end up securing the house. I want to share with you a few tips that help make this happen.

Firstly, I think getting the right Realtor® working for you will be the most important step. Someone who can be a guide through this complicated process. A thorough review of the market is also very important. Often times multiple bids are created because a house is under-valued as compared with other listings that have sold in the area. This means that even though a buyer might pay more than list price for a home they are not necessarily paying over market value.

Price is often the most important factor in an offer, but not always. For most people, there is a human element in selling their house. I like to present my offers directly to the seller in multiple bids. Basically, tell them how wonderful my clients are-which is usually true! I have had sellers more than once choose my clients’ offer that was less money. One time over $3000 less!

Conditions also play a factor. Having too many conditions or long timelines can make an offer less attractive. In some cases, If the house is perfect then I suggest a pre-offer inspection. This way we can put forward a firm offer when the bid time comes. This will strengthen the offer considerably.

Multiple bids will always be a part of the home buying process. You might win some or lose some. Just remember things always have a way of working out in the end. If it is meant to be it will be!

Posted on: July 10th, 2017 by Chris Scott

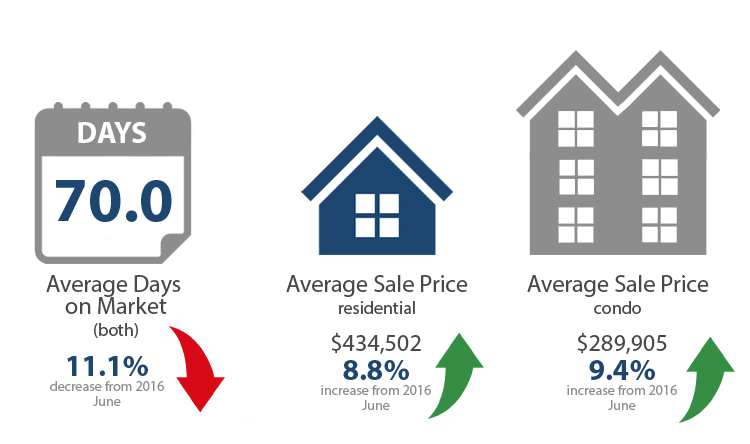

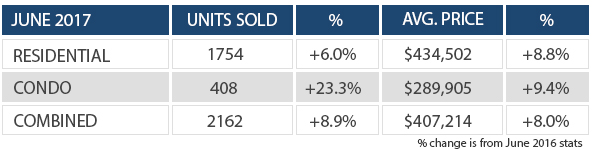

Ottawa’s market has been thriving for the first half of 2017. Month over month we are seeing an increase in units sold and average sale prices increasing from last year. Compared to last year at this time, Ottawa homes sales units in both residential and condos property classes are up 13.5%. The average residential sale price for June 2017 was $434,502 up 8.8% from last year’s June and the average condo sale price for June 2017 was $289,950 up 9.4% over last year’s June. The number of Condo units sold per month continues to stay strong with an increase of 23.3% compared to last year’s June. This is the 5th year in a row the number of units sold both residential and condo properties have increased in June. The demand is still high right now in certain neighbourhoods. I predict that in the second half of the year we will continue to see record-setting prices for units sold and average price.

Posted on: July 7th, 2017 by Chris Scott

Last week MoneySense magazine announced the best place to live in Canada. No surprise to me that Ottawa reigns as number #1. Back to back champs!

Based on employment rate, household income, health, weather, crime rate, transit and much more Ottawa has been ranked the best place to live in Canada 2017. Ottawa is not the boring government town we have been labelled as in the past. Honestly, I’ve never felt that way about Ottawa myself. There is so much culture here and frankly being the best city in the best country is pretty good. Real estate is also reasonably affordable if you consider just how good we have it to live here.

With the new successful development of the Landsdown Park and our Grey Cup Champions Ottawa Redblacks, it is has brought lots of new fun and excitement back to the city. This year with the Ottawa Senators making it to the NHL semi-finals the cities energy was at an all-time high.

Ottawa has something to offer everyone each weekend. Events we love such as Bluesfest, Winterlude, Busker Festival, Tulip Festival or yoga on the hill and skating on the canal, how could we ever be called boring? On top of that, only 20 min outside of the city is skiing, hiking, and beautiful cottage country. We love our city and we are not surprised to be ranked #1 two years in a row. #WeLoveOurCity #ProudOttawarian

Posted on: July 6th, 2017 by Chris Scott

MISSION

To completely stage a Barrhaven single family home and have it launched back on the market within 24hrs.

I got a call one morning from someone who had their house listed with a limited service brokerage. They were super unhappy and wanted a change. I met with him almost immediately. He offered me the listing if I was able to do the impossible: completely stage and reposition them on the market in 24 hours. This process usually takes at least a week! They wanted to have it back on the MLS ASAP to take advantage of the busy Ottawa spring real estate market. I decided to accept this challenge.

STAGING

We had an interior decorator at the house for 7 pm that evening. The staging was completed at 10 pm and the sellers told me they stayed up well past midnight implementing the changes. The next morning our staging expert was back putting the final pieces into place. We had our media company into the home for pictures and launched on the MLS shortly thereafter. This was by far the quickest turn around I have ever had.

RESULT

My clients had their house on the market a total of 2 days with me and we sold their home in a multiple bid situation for full price! The price was $5000 more than my client’s original asking price. The house was previously on the market for 2 full months without an offer. It matters who you work with!

LESSON

VALUE IS MUCH DIFFERENT THAN PRICE. It is easy to be lured in by saving money by listing your home with a limited service company. I get it, it is human nature to want the best deal. However, the best price is not always the best deal. This is true with almost everything we buy. In real estate, the best deal is whoever can put the most amount of money in your pocket after expenses while making the process. In this case, we were able to accomplish this objective for our clients.

If you are selling your home in Ottawa give us a call. We will get you the most money with the least amount of headaches. But please give us more than 24hours to prepare the house 🙂

Posted on: June 6th, 2017 by Chris Scott

RAINING SALES IN OTTAWA

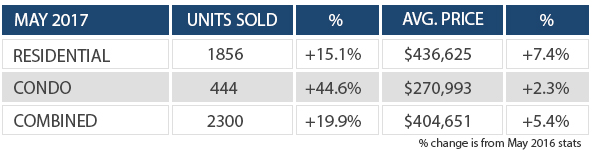

It was raining sales in the Ottawa real estate market last month. Amid one of the rainiest months ever, we also experienced the busiest real estate market in Ottawa history. We absolutely shattered the previous record by over 315 units. The Ottawa residential market has been hot for a while now but the condo market is also coming alive which is leading to this extremely active market. Condos sales activity is up 44.6% over May of last year. In total 2300 units were sold last month! That is up from 1919 units sold in May of 2016. This includes both condos and residential freeholds.

In most neighbourhoods, Ottawa is in a seller’s market. There is just not much inventory and lots of demand. Multiple offer situations are very prevalent in the central neighbourhoods. Freehold prices are up 7.4% over May of 2016 while Condo’s are up 2.4% over May of last year.

Now more than ever it is important to get the advice of an agent. Pricing/marketing strategies are different for every neighbourhood. If you are interested to see what your home would sell for in this market please feel free to get in touch.

If you are curious about your homes worth please fill in this form for a no-obligation market assessment.

Posted on: May 26th, 2017 by Chris Scott

Home staging is such an important aspect of selling your home. In Ottawa, home buyers have lots to choose from. It’s important to make the right first impression. These Ottawa sellers worked with our staging team to make sure their house sparkled when it hit MLS. They ended up selling in a week for 99.8% of listing price. As you can see this hard work staging paid off for these clients.

Create A Unique Space

The dining room just needed a few large accessories to give it impact. For our team, the biggest difference was adding the drapes. It helped define this space as a separate room. The living and the family room both had the matching filtered blinds so having the drapes in this room made it different. It was also another way to bring texture and colour to the room.

Living in a Staged House

This can be hard when you have young children. The goal is to make it looks it’s best so it sells quicker and you can resume your ‘normal’ living. Removing the toys made a huge difference and it elevated the look of sophistication in this house. Look how beautiful the floors are. You always want to showcase the beauty in your home.

Time to Borrow from Family and Friends

We were very lucky that their friends were kind enough to lend them their sofa. It is very understandable if sellers don’t want to buy furniture if they don’t know what they are moving to. We ask sellers to borrow from family and friends if possible. The whole purpose of Staging is to keep your costs down, for the most profit.

Posted on: May 5th, 2017 by Chris Scott

Our staging team last month did an extraordinary job transforming this home. Having the rooms painted made a significant difference in the results. Check out the before and after pictures below.

As our staging team walked into this house back in December, we knew it needed to be painted. The homeowners were very reluctant and it took some convincing that they would get their money back in the paint. We are happy that they decided to go ahead with it and hire professional painters to make sure the job was done right. These homeowners were amazing to work with. They did whatever we asked them to do and were more than willing to buy what we suggested. Once the painting was done, we were surprised how quickly we could turn it around.

Neutral Walls and Furniture Placement

The living room walls made the room feel small and dark and their U-shape sectional dominated the room. When homeowners get transferred around a lot for work, it can be challenging for them to know what furniture to buy, that will fit in other houses. We also felt that the TV dominated the room.

The neutral walls completely transformed the room. We needed more furniture for the office loft, so moving part of the sectional upstairs enhanced both rooms without costing anything, They also switched the large TV for a smaller one that they already had. We love the challenge of rearranging the furniture in different rooms to repurpose it.

Removing the white floor lamps with a stylish table lamp softened the room. Their new gray shag carpet is something that they will be able to use in their next house. It adds texture and expands the space making the room feel larger. Notice they even spray painted the brass around the fireplace with BBQ heat retardant paint.

We brought in large artwork to tie the whole main living space together. You are always better with fewer larger pieces than several small pictures for Stagings. Their new chair invited you into the room and created a welcoming space for conversation, not just TV.

Dining in Style

We were concerned about painting these gold walls since they were ragged with glaze and had texture. This could really scare off buyers. This is why we were so happy they hired professionals. They also had too much furniture in the room.

Once the large cabinet was removed, they were able to turn the table to the other direction. This made it mush easier to walk around. You only need a few large accessories to give some drama. Removing the valance from the window also updated the look.

Kitchen Cabinets

Replacing or even painting kitchen cabinets can be risky since you really don’t know what buyers are going to want and it’s an expensive task. It’s safer to just make them look their best. These cabinets are in perfect condition so it would be a shame to change them unnecessarily.

The new wall paint colour worked with the floor and neutralized the colour of the cabinets.

Tone it Down

The office/den room was a catch-all room and we really wanted to give it a purpose for resale. We moved this futon downstairs in the family room, removed all the storage bins, brought in a desk and continued the same paint colour upstairs.

Buyers can see this as a home office, a guest room or den. The homeowners’ had their father’s photography blown up as a surprise. We love it when you can still personal touches in a house.

Work With What You Have

When our staging team walked in, this children’s room didn’t make sense to me. It had adult furniture but a youthful painted mural. This mural was here when they bought the house. They didn’t have any children but one of their relatives had a crib that they weren’t using.

Now, this room looks like an adorable nursery that might just be the selling feature. If buyers don’t like it, they can always paint over it but it was faster for us to just put in the crib, remove the other furniture and put up some white drapes to keep it looking fresh. The crib also makes the room feel larger than a queen size bed.

Master Bedroom Gets Some Drama

They were already starting to pack up some of their things. New drapes, linens and artwork were the biggest change in this room. They didn’t have a headboard but this canvas artwork creates the illusion of one and gives the bed some height. The matching lamps also give symmetry. The turquoise drape panels on both windows extend the colour to the far end of the room. A few simple accessories give the room atmosphere. The round shape of the mirror softens all the edges of the room.

Posted on: May 5th, 2017 by Chris Scott

The balanced market of the past few years has seemed to evaporate overnight. The market is extremely competitive right now in Ottawa. A shortage of good inventory and favorable demand has shifted the balance towards the sellers. Bidding wars are once again a common practice here in Ottawa. The exception this year is that some of the bidding wars are escalating high above the listing prices. In one instance I witnessed a home sell for 100k more than a sellers list price. It started in March and was mostly contained to the central urban market. Neighbourhoods like Hintonburg and Westoboro are especially hot. That heat has extended to the suburban market, It is not as active but in some segments of the market, every well-priced home is in multiples. As an example, it took my clients 5 offers to secure a Kanata townhouse. They were over asking on all 4 of the previous bids. Every neighbourhood has different trends. Much it will depend on the available inventory in each area. Comes back to simple economics sometimes. Low supply + high demand = Craziness in the Ottawa market.

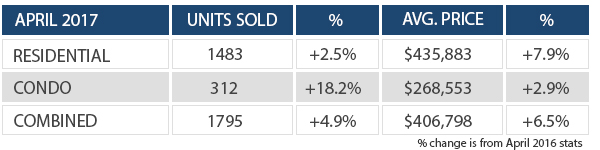

Let’s examine the April resale numbers for the Ottawa market:

This upwards push is fuelled by a combination of high consumer confidence and good local economic conditions. Houses sold over 1M doubled this April compared to last year. There were over 83 properties sold in the 7 digits! This is an interesting trend to keep an eye on. If you have questions about your neighbourhood trends feel free to get in touch.

Posted on: April 5th, 2017 by Chris Scott

The Ottawa Real Estate market is heating up. Price gains for both residential and condo units are up 5.3% year over year. The average sale price of a residential property was $415,467 and $272,597 for condos. Sales are up 28% over last year and we are just shy of the all-time record for March sales.

The core of the city is as active as I have seen it in years. There are limited inventory and lots of demand. This has created many situations where sellers are getting much more than asking price. In one instance I witnessed a home sell for 100k over asking price. It is a challenging market for buyers right now. Especially in the areas around Wellington village and Hintonburg. These areas are experiencing multiple bids on almost every house!

In the suburbs, the economics are more balanced. There is a reasonable amount of inventory and multiple bid situations are rarer. However, it is more active than in years past. It is going to make for a very interesting Spring market. The traditional busy season is still yet to be upon us.

The market has different patterns depending on your neighbourhood and category of home. If you are interested to know what’s happening in your neighbourhood, feel free to get in touch.